-

TrendsEuropean Affairs

-

SectorHealthcare and Pharmaceutical IndustryIT and Communications

-

CountriesGlobalSpain

INTRODUCTION

Humanity may indeed have developed some formidable technologies for accumulating information, but the truth is, our memories remain very short. It has only taken two or three generations to forget about the consequences of the poorly named “Spanish flu” that killed hundreds of millions around the world between 1918 and 1919. Tragic loss of life aside, that pandemic went on to revolutionize many aspects of society, culture and the economy by introducing structural changes in the ways people lived. We need look no further than Spain to see that it accelerated the role of industry, thus raising the country out of a farming economy; forced a transformation of waste management systems, which did not exist as they do today; and changed the way cities were designed, introducing large plazas to avoid crowds. Some studies even suggest that the pandemic had a decisive impact on World War I. With death and disease among hundreds of thousands of soldiers accelerating an end to the fighting and forcing a bad peace treaty (Versailles), which simply led to a second World War 20 years later.

We forget that, 100 years ago, a virus came and changed almost everything. History is repeating itself now, and a new virus has arrived in 2020 to shake up a society that we already thought was moving fast. Or so we believed, from atop our tower of stability. A fluid society and constant uncertainty loom over the horizon, and our ingenuity is only now being revealed.

With a hard lesson in humility under our belts, this report tries to highlight the big conversations we are seeing take shape. Some are mutating into something else, and several more we strongly doubt will remain as they are today. All of these conversations are and will be undoubtedly digital, because that is an inherent condition of conversation itself in today’s world.

Seeing the bigger picture may help readers navigate the rough seas of decision-making that surround the issues impacting business: Where might regulatory decisions take us? What are my consumers concerned about? And what issues should I focus on in my relationships with my stakeholders? Nobody has all the answers, but we may be able to find a few of them together if we start here.

Maria Branyas is the oldest person in Spain. She is 113 years old. She lives in Olot (Girona, Spain), and she has just recovered from the coronavirus. She was born in 1907, so she also lived through the Spanish flu as well. She recently said, “From the solitude of my room, fearless and with hope, I don’t really understand what is happening in the world. But I don’t think anything will be the same again. And don’t think about redoing, recovering or rebuilding. Everything will need to be done again, and done differently.”

Everything will need to be done again. We should listen to our elders.

To develop this report, we conducted 62 vertical analyses of territories and communities on Twitter (a total of over 180 million tweets), and we monitored trends over time in search frequency for keywords and key issues on Google regarding the territories of interest.

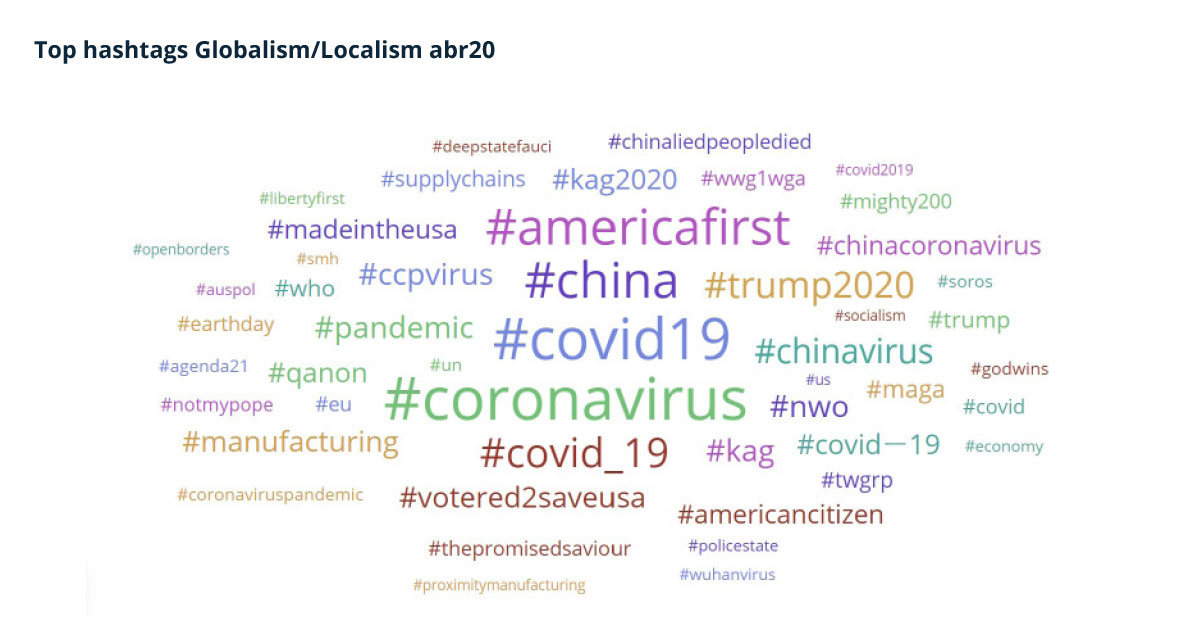

1 GLOBALIZATION VS. LOCALISM

The breakdown of globalization as we have known it for the last few decades has been in the cards since the 2008 financial crisis. Perhaps the coronavirus pandemic is the killing blow. International trade’s expansion era had been dwindling since the beginning of the trade war between the United States and China, initiated by tariff impositions and departures from international agreements. Now, supranational organizations have been unable to show usefulness in building a coordinated solution to the pandemic, which will leave serious wounds on multilateralism and international cooperation. This will be further exacerbated by national protectionist ideologies.

The following months may put into question the ways major corporations function, as well as their very natures. The pandemic has lent support to the protectionist and nationalist arguments (albeit for different reasons) of certain political leaders, such as Trump and Bolsonaro, by firmly committing to industrial sovereignty over production and value chains. Whereas Twitter conversations in this territory in April 2019 were full of hashtags about Brexit and Trump’s nationalist posturing, COVID-19 and references to the supply chain are gaining popularity in the same period in 2020. These are interspersed with political slogans, and a more complex and argued conversation is being constructed.

The pandemic has driven conversations about company value chains toward a focus on greater resilience based on supplier diversification, as well as greater digitalization. This will enable them to deal with future disruptions. Beyond the structural effect on supply chains, however, the COVID-19 effect has another short- and medium-term impact: International tourism. It may be safe to assume that the mobility restrictions will be temporary, but we are facing a period in which action protocols and fear of contagion will be the main barriers to overcome: bureaucracy, social distancing, order, waiting, processes… The free will normally associated with tourism will continue to be constrained. In this reconfiguration, the most-developed countries could have an advantage in terms of demand when compared to exotic destinations, as healthcare systems are often less advanced in this locations, affecting travelers’ perceptions of safety when they choose to go on holiday.

“The pandemic has driven conversations about company value chains toward a focus on greater resilience based on supplier diversification, as well as greater digitalization”

While the COVID-19 effect enables a reduction in the trade of physical goods and individual mobility, digital globalization might well gain popularity. Online relationships and services have demonstrated strength during this crisis, with teleworking at the top of the list. Nonetheless, this will be accompanied by the first major consequence: A reemergence of localism in an inverse process of globalization. The bureaucratic burdens on the exchange of goods and people are leading to attention and concern for what we have close by, including our neighbors, local produce and news from our own neighborhoods. All things nearby have proven useful and tangible during this crisis, which has contributed to a reassessment of the local social fabric. Neighborhoods are now leading the new scale of how service integration and emotional connections are measured.

2 THE WELLBEING REFORM

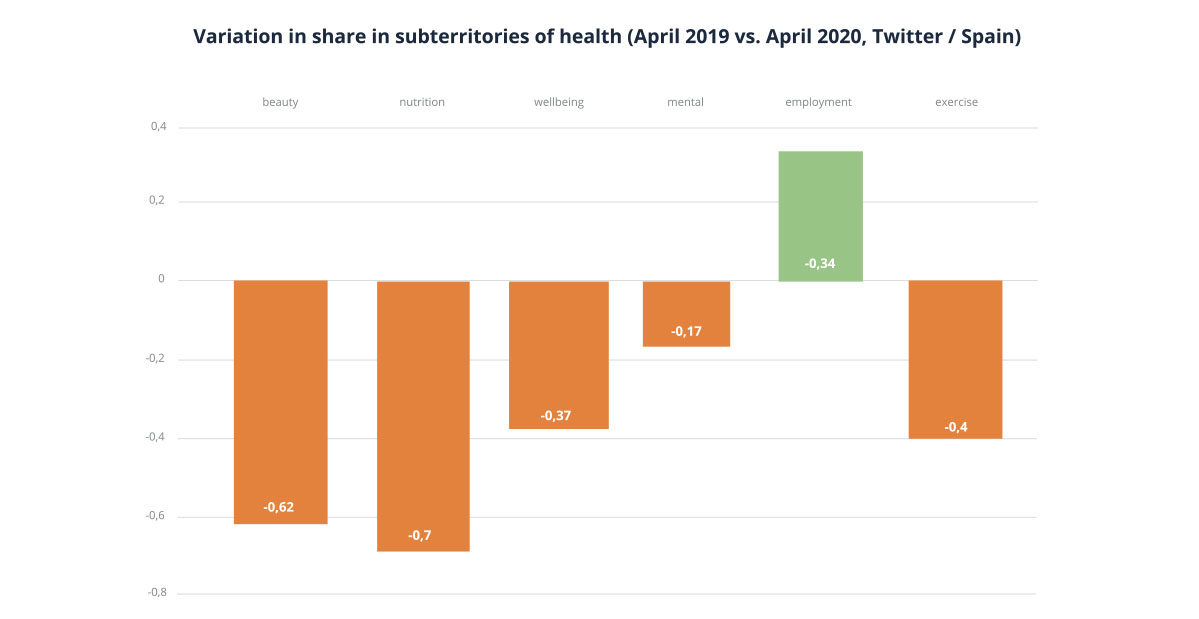

This pandemic has profoundly rearranged Maslow’s hierarchy of human needs, built after the end of World War II. We are returning to needs we thought long since overcome, such as the need for physical safety and health, which are perhaps even more basic than the need to breathe – after all, we are sometimes scared to breathe in certain places. Therefore, the post-COVID concept of wellbeing has been widened at the base, and these needs rise to the same level as personal care, aesthetics and nutrition. We can see it in the figures: Conversations about beauty have fallen by 62 percent when compared to last year; those about are down by 70 percent and those on wellbeing by 37 percent.

Furthermore, one subject that had been sidelined from the public agenda for too long has returned with force, and it is considered by many studies to be the next major challenge in healthcare management: The population’s mental health in a post-traumatic situation.

Three important conversations on the topic of wellbeing are highlighted below:

- Mental health: The WHO has warned that confinement measures will increase depression and suicide rates among populations. Talk in the United States is already focused on a mental health pandemic over the next two years, with a high number of anxiety-related cases stemming from employment instability and uncertainty. One of the most interesting issues will be how companies and organizations protect and cultivate mental health among their employees. The national health system will also be a subject of major debate because, although there is agreement about the need for it to be underpinned, solutions are numerous, complex and extremely expensive. Governments are clearly not prepared to deal with a mental health pandemic.

- Solidarity and cooperation: Returning to more basic principles can also mean increased cooperation. This risk to collective health has demonstrated the strength of social networks in guaranteeing the population’s survival and wellbeing. It is very likely we will continue seeing social and business initiatives based on cooperation, support and solidarity.

- The new wellbeing: Industries related to physical care and beauty will evolve to incorporate health and hygiene into their business models. However, we may also see major impacts on areas such as architecture or urban planning in terms of how spaces are constructed and common areas used to create richer, more well-adapted and healthier environments. There will be new opportunities for the care industry, beauty, fashion, architecture and industrial design in developing new business and social networking models.

3 SENIORS AND THE IMPORTANCE OF CARE

It reads like a fiction story. Two months ago, we thought of the Baby Boomers (active people over 60 with savings for whom their age was not an issue) as a driving force behind the economy due to their investment in leisure and wellbeing, especially now that life expectancy is longer. However, there’s nothing better than a dose of reality to put us in our place and force us to see the other side of the debate around seniors: Care.

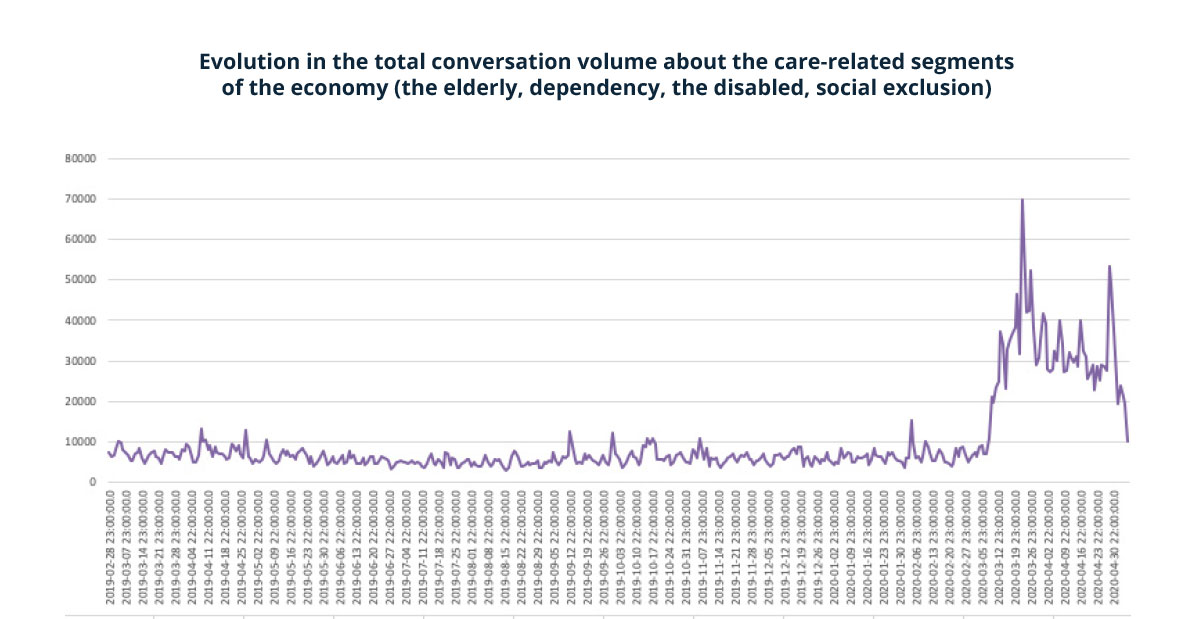

Whether paid or not, care will be a major social issue in the years ahead. The crisis, combined with the 18,000 elderly people who have died in care homes and this population’s extreme vulnerability to the virus, has proven how important an integrated care policy could be. The care economy accounts for 15 percent of Spain’s GDP. According to the ‘Care Work and Care Jobs for the Future of Decent Work’ report by the ILO, “changes to family structures, higher care dependency ratios and changing care needs, combined with an increase in the level of women’s employment in certain countries, have eroded the availability of unpaid care work and resulted in an increase in the demand for paid care work.”

Looking at the figures, the care world may simply be seen as another area undergoing a transition process, moving from unpaid work by family members to paid work from outsourcing this care, and that the three pitfalls, two pending reforms and change of mentality listed below must be addressed.

The three pitfalls we may encounter are:

- A new social class, but the same precariousness

According to sociologist Maria Angeles Duran, a new social class of caregivers and receivers has been created. She describes it as “an emerging social class consisting of ‘those who care,’ usually women who look after dependent elders without pay, rights or visibility.” This segment also includes a high percentage of care recipients (more than 2 billion people) with a not insignificant impact on GDP (15 percent and rising). A 100 percent investment in this field could lead to the creation of 1 million jobs, which sounds like heavenly music in a situation such as this. But what sort of jobs are we talking about? Precarious, non-professional and unstable ones.

- Relief for families

Paid care work seems like a relief for families suffering from a loved one’s situation of dependency. However, the reality involves feelings of impotence, frustration and enormous guilt, which the news in recent weeks will only continue to highlight. In this Catch-22, it is just as bad to outsource the help (guilt) as it is to not provide it (impotence). Dependency as the fourth pillar of the Welfare State is another of the pitfalls to navigate.

- The gender issue

Unpaid care work is mainly carried out by women and, when talking about women’s access to the labor market, one of the main gateways available to them is care work. So, women often provide care altruistically and do so precariously. It is a vicious cycle.

The two pending reforms are:

- Welfare State and pensions

Over the coming months, we will be hearing a lot about how the Welfare State and pensions system need to be reformed. In Spain, the dependency rate is projected to rise to over 60 percent by 2033 and 75 percent by 2068. The existing productive system will not be able to meet the costs of such a brutal shift in the population pyramid.

- Coordination between authorities and public-private partnerships

Among this crisis’ many lessons is that the answer involves greater system transversality, from exchanging information to coordinating measures, optimizing resources and centralizing procurement. If viruses recognize no borders, policies to deal with them shouldn’t either. Nonetheless, this reform is unlikely to take place.

“Whether paid or not, care will be a major social issue in the years ahead”

The change in mentality about/toward the elderly involves reconsidering the value and meaning of life. With 30 percent of the world’s population projected to be over 65 in 2100 and a growing life expectancy, society’s mental map of opinions about the elderly will need to be reconfigured. The meanings of life, work, leisure and all things aesthetic, as well as sexuality and identity, will need to be transformed over the coming years.

Organizations will be forced to reconsider their roles, with a focus on not only the adaptation of assets and services, but also on social contribution, including the importance of care and how we interact with one another in our most immediate environments. Consumers are looking to find a framework brand values that forms an active part of the solution. Usefulness, generosity, commitment and the need to help one another is the new language for companies seeking to connect with people.

4 CRACKS IN EDUCATION

Education is another area that has been thrown up in the air by COVID-19. Nothing about this situation is new, but what feels like five years have passed in a matter of weeks. We will be talking about education a lot, and we will be talking about an education system that is expected to produce resilient and employable citizens. Resilience is the new humanism in an education sector fighting for the competitiveness of its offering while trying to manage five deep cracks.

Breaking away from physical spaces

In this COVID-19 crisis, 91 percent of pupils around the world (equal to 1.5 billion children and young people) have been forced to start learning from home. Technology has proven to be an essential ally in keeping up with classes, leading to an access gap of around 10 percent in compulsory education and 3 percent in university education in Spain alone. Blended face-to-face and online learning has received the backing it needed over the last few weeks, and everything suggests that the 2020-2021 school year will be its debut year, although regional government authorities, schools and parents are showing reticence toward a model that has not yet been proven to work.

Breaking away from the figure of ‘teacher’

Educators have been going through a process of trial and error for years. Conventional classrooms don’t work, and neither does conventional teaching. Memorization has been left behind, and gamification and shared knowledge have taken its place. From the all-knowing teacher, we have shifted to answers being available everywhere at the click of a mouse. Students no longer needed teachers to acquire knowledge. Even so, teacher figures are more important than ever. Therein lies the challenge.

Breaking away from knowledge

This is all because education is also now a combination of skills and abilities. Knowledge, as static and linear boxes, has no value in a world that is constantly on the move and transforming. Functional, emotional and resilient citizens capable of understanding the complexity of its contradictions; of developing technical, applicable responses; of exercising emotional intelligence both on their own and with others; of being creative and collaborative are the new “Michelangelos” of this world. Now that we are physically distancing ourselves from one another, it is more important than ever to build a community.

Breaking away from qualifications Education used to be a continuous line, accumulative and limited by time. The concept of lifelong learning emerged as a figure of speech, but it eventually took hold to become reality in most productive sectors. Long and linear academic careers will not be competitive. Rather, pill-based learning with practical seminars, anti-master classes and short bursts will be what improves our functionality, capable of fitting into our professional and family lives while limiting the onset of obsolescence. This has led to the success of MOOCs (Massive Open Online Courses) and progress towards a singularization of education.

Breaking away from the promise of equality Education will be experience-based, achieved through the use of artificial intelligence and virtual reality. This won’t happen immediately and will take place at different speeds, leading to numerous debates around equal opportunity (perhaps the most relevant topic in the field of education) and the supposed “unfair” competition from new players in the sector (mainly technology and entertainment operators and platforms). The problem lies in the widening gap between economic classes and the disincentive the most vulnerable parts of society will feel toward education, with a growing trend of leaving school early. This will be seen in the dichotomy between public and private, between science and the arts, between central and peripheral. Each one of these cracks is opening an equal opportunities gap that can only be faced through state policy that understands education as a lever for national competitiveness.

5 THE DEFINITIVE REINVENTION OF ENTERTAINMENT

This crisis has poured more fuel onto the fire in the entertainment industry, accentuating the problems and opportunities stemming from digitalization and the democratization of production and access to content. The conflict between digitalization and face-to-face experiences has heightened existing tensions between traditional industry models (based on controlling content licenses and their broadcast times) and new methods of consuming media. In the audiovisual industry, those who will suffer the biggest loses from COVID-19’s impact will be the cinema screening chains, which have been fighting against new over-the-top (OTT) players, such as Hulu, Netflix or Amazon Prime Video, over screening windows for the past several years. Movie theaters now see their business being damaged not only by audience perceptions of insecurity, but also by the consolidation of on-demand consumption in people’s homes. Most of the big players in production and distribution have sufficient streaming windows to make their products available to audiences, even during a pandemic situation like this. This situation is forcing the traditional screening industry to reinvent itself or possibly even ally with its competitors. This has been furthered by major events and awards, such as Cannes or the Oscars, which are starting to open their doors to new formats in their selection and screening criteria.

“This situation is forcing the traditional screening industry to reinvent itself or possibly even ally with its competitors”

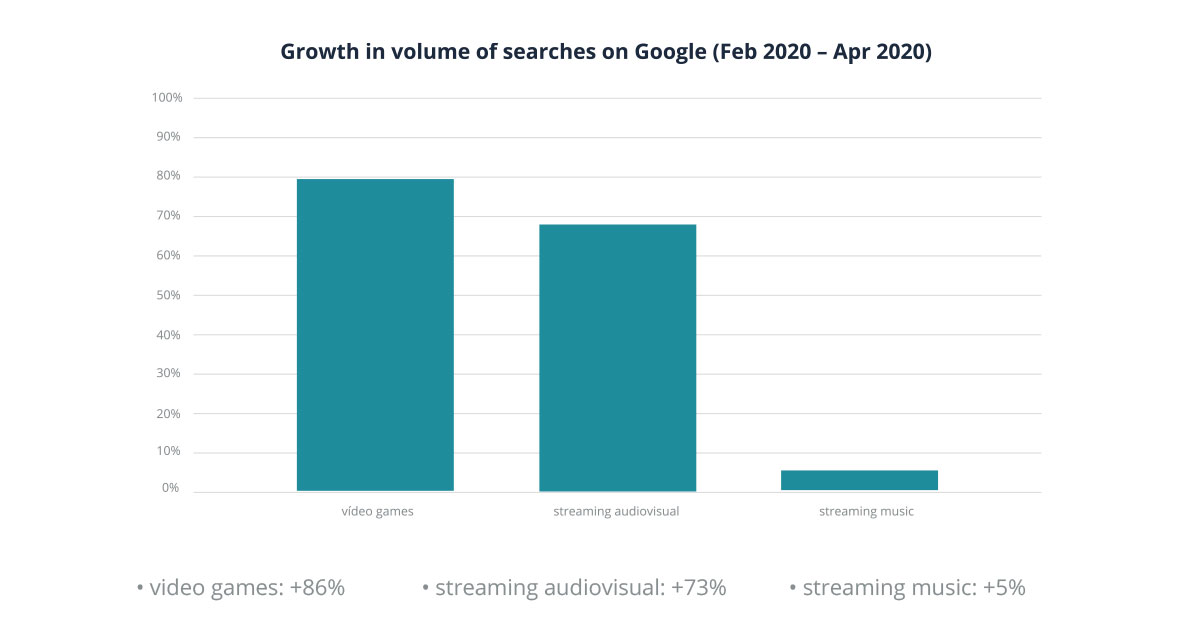

The problem is multiplied in the music world, which was already being dragged down by far more serious endemic problems. The industry already struggles with being unable to find a sustainable model that would allow them to survive while also responding to the realities of modern consumers. Until now, the streaming model sought to replace the traditional one, ruled by record labels that mixed artist management with a focus on live performances. Artists tend not to support switching to selling licenses to streaming services due to how little they are paid for it. However, while the rate of audiovisual content consumption on streaming platforms has continued to climb during the lockdown, the consumption of music on players such as Spotify or Deezer has fallen. This is coupled with disaster in the live performance industry, which will take far longer to recover given the difficulty of safely running concerts or festivals like the ones we’ve enjoyed up to now. The music industry, which was still trying to adjust to the digital age in 2020, will need to completely reinvent itself due to the effects of COVID-19.

In turn, gaming (which the cinema and TV series industries see as the main competitor for consumer attention) is coming out on top during the pandemic. However, that triumph is being offset by the growing e-sports industry’s excessive dependence on large-scale events, which had previously been the main focus for brand investment. The vacuum created without these events is an opportunity for publishers and broadcast and conversation platforms such as Twitch, which brands had not utilized until now.

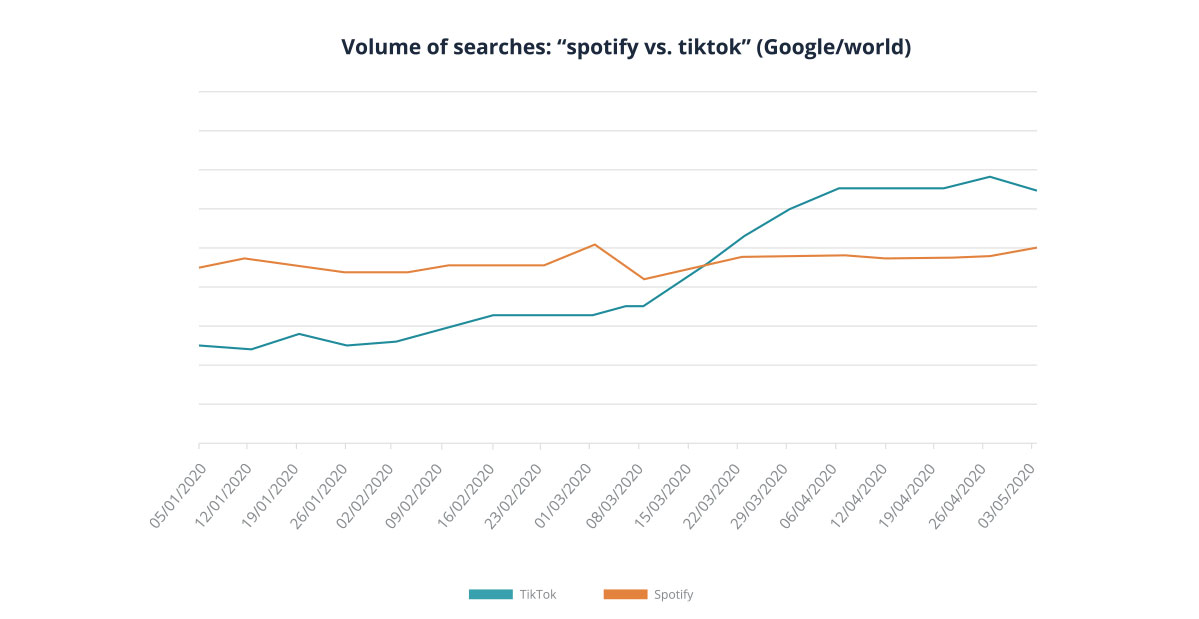

This pandemic leaves us with an entertainment industry that will need to accelerate its digital transformation and overcome its excessive dependence on face-to-face experiences. They will be competing with the rising production and consumption of user-generated content, with platforms like Tik-Tok gaining traction. The emergence of useful entertainment, with a special focus on wellness content, will also provide brands with food for thought. Until now, brands have been highly focused on traditional sponsorship models that focused on major physical events. Diversifying away from this model will create even more opportunities for branded content.

6 GREEN ECONOMIC RECOVERY?

Over the last decade, strong progress has been made in terms of raising awareness about climate change. The ecological agenda has made in-roads into politics, the economy and society with a rare level of efficacy thanks to strong warnings from civil and scientific organizations regarding the climate emergency we face. Following the Paris Agreement in 2015, which offered the first global framework for reducing greenhouse gas emissions, the countries involved got to work and were making significant progress. Then came COVID-19, which has put the whole world on pause. In a scenario of economic recession, classic economic theory leads us to conclude that private investment will slow, especially nonessential investment. Similarly, the expectation is that governments’ ecological agendas will need to be less ambitious, and issues that increase pressure on companies (such as green taxation or political incentives) will be relaxed.

Contrary to this theory, we are seeing a growing phenomenon of pressure to intensify these practices, which may position the ecological revolution as a lever for economic reconstruction. Several European countries have already signed the Green Recovery Alliance. In turn, the European Commission itself has positioned its European Green Deal project as one of the most powerful reactivation tools. The Spanish government also seems to be heading in the direction of ecological reform: It is working on a growth and progress model based on balanced use of renewable resources and on recycling nonrenewable resources. There will, of course, still be a great deal of disagreement with extreme positions on the ecological transition as policymakers seek to leave room for measures that alleviate the economic stress placed on companies.

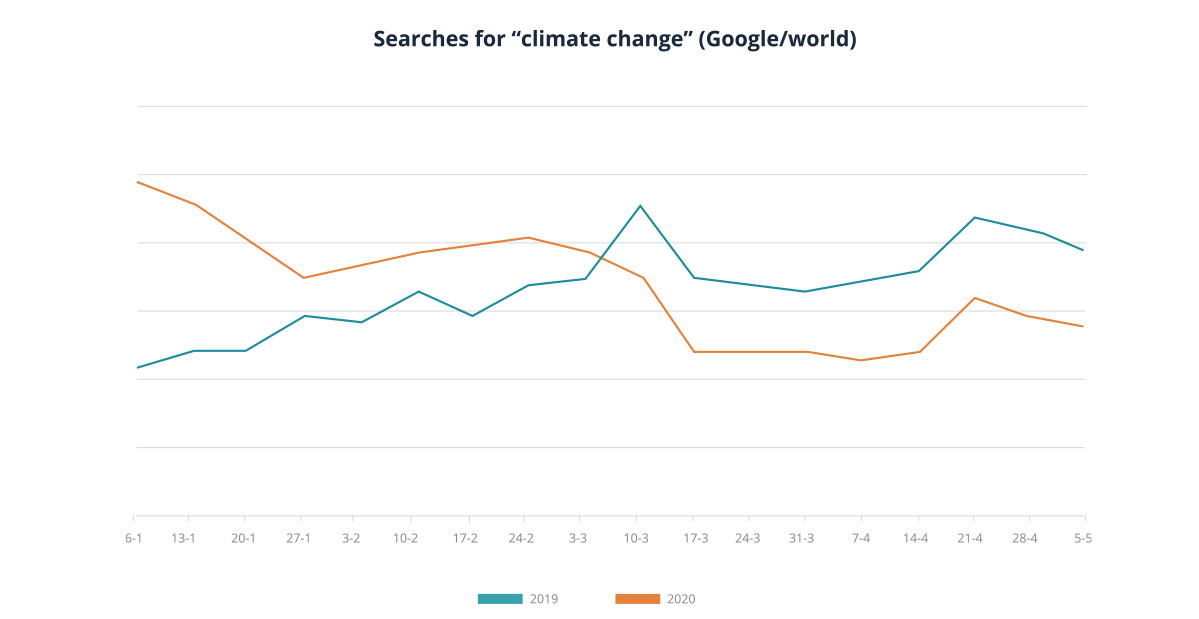

For the time being, conversation analysis shows a sharp decline in conversations about sustainability and climate change. That is entirely to be expected, as COVID-19 dominates online conversation. When we return to a certain degree of normalcy, perhaps we will see a more polarized conversation. Supporters of the ecological agenda will likely present it as the right way forward, while other groups may become more active in defending the economy/ecology dichotomy.

That same ecological tension can be seen in other layers of the conversation. Many companies will find support for their green positions under these circumstances, and it may be a way to stand out in their category: Fewer processed foods and products, more sustainable production and commercialization processes. This can turn into conversations about how this health crisis is returning our attention to nature and highlight the importance of buying better quality products, even if they are more expensive. However, the economic recession is making buying sustainable products less accessible, as these products are also less affordable.

Plastic products and packaging are an example of this battle. Disposable plastics have proven extremely important to preventing the spread of disease amid a global push to discourage their use because of how they pollute the environment. It is likely that plans to impose a tax on disposable plastics will be delayed, but will eventually move forward. Manufacturers will become polarized, shifting into those that delay their own green revolutions and those that accelerate it because they see it as a commercial opportunity.

“When we return to a certain degree of normalcy, perhaps we will see a more polarized conversation. Supporters of the ecological agenda will likely present it as the right way forward”

Authors

Carmen Muñoz

Daniel Fernández Trejo

Guillermo Lecumberri

Miguel Lucas

Carlos Ruiz Mateos